The recent US inflation update, which saw consumer price rises fall to 3.4% and match expectations for the first time in five months, sparked relief among investors. Following a weak April, when equities appeared to be losing steam, stock markets climbed to all-time-highs with the S&P 500, Nasdaq Composite and Dow Jones Industrial indices all breaking new ground.

The positive sentiment stemmed from interest rate cuts returning to the agenda for 2024, allaying recent fears that stubborn inflation may see them delayed until next year. Although unlikely in June or July, the US futures market is once again predicting two cuts of 0.25% each by the end of the year.

In the Eurozone, where inflation has dropped to 2.4% and the impact of Red Sea trade disruption is now expected to be less harmful than previously thought, the ECB looks increasingly likely to start cutting next month, with three further reductions anticipated before the end of 2024.

As well as inflation falling towards central banks’ long-term targets, there are encouraging signs that the global economy is on track to keep growing. Recent employment and PMI data has been positive while the latest Bank of America global fund manager survey showed that over three quarters (78%) of respondents think a global recession unlikely in the next 12 months.

Tech time bomb still ticking…

The same survey revealed that investors are the most bullish since November 2021 but history has taught us – particularly those with a contrarian mindset – to be wary when such optimism fills the air. The main threat continues to be concentration risk in US equities, albeit one that can be mitigated simply by investing away from the index where the largest seven technology stocks now represent over 30% of its total weight.

The US technology sector is currently priced at 33x earnings – 83% above its 20-year average (18x) and a valuation last seen in 2002 when the IT bubble burst. This has swelled the S&P 500 index to a forward P/E of 20x – a level where subsequent 1-year returns have tended to be negative and 10-year annualised returns have always been lacklustre (2-5%).

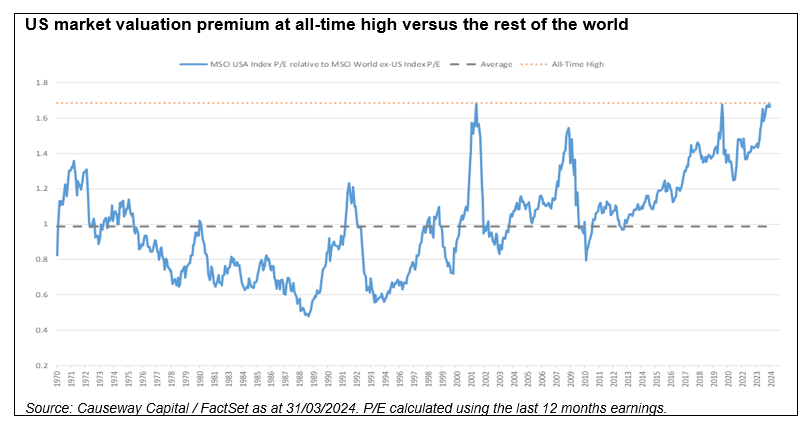

Relative to the rest of the world, the US is currently priced at a record premium on an earnings basis, with Europe and China priced at discounts of 30% and 50%, respectively. Emerging Markets generally offer good value with all major developing countries except India and Taiwan trading below 20-year average valuations (P/B).

Where next?

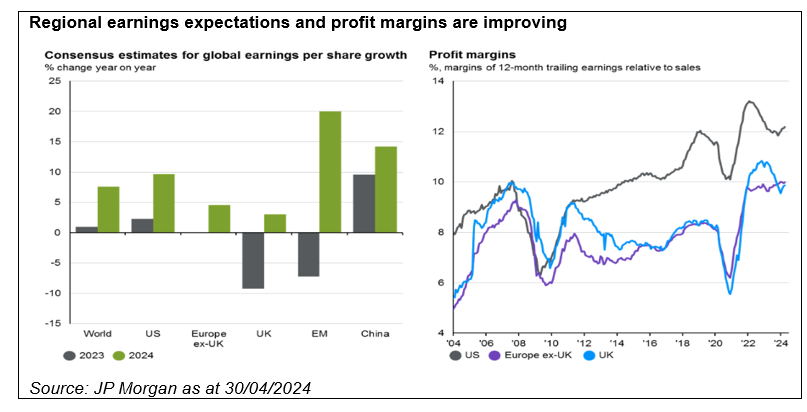

The current environment of positive economic growth, higher-for-longer interest rates and reasonable valuations (outside US tech) should be favourable for value stocks whose earnings and valuations tend to benefit most from a cyclical recovery. Consensus forecasts show that corporate earnings are expected to improve across all regions this year, while margins are also improving.

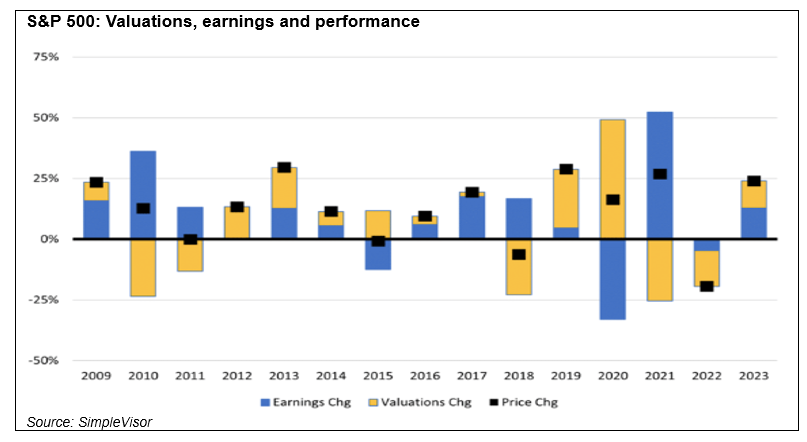

So, what does this mean for stock market returns? Over the long-term, valuation is the main driver with multiple expansion or contraction dictating equity performance, regardless of earnings or margins. The chart below shows how changes to valuation and earnings have contributed to the S&P 500 return each year since the financial crisis. For example, the index was up 24% last year with rising earnings and increasing valuations contributing equally.

If the current P/E multiple (20.1x) remains unchanged, the price change will equal the growth in earnings, which is expected to be around 10%. If the earnings multiple falls towards its 10-year average (17.7x), however, then the price will be broadly flat, a situation similar to 2011.

Although less important than valuations over the long-term, earnings are important for sentiment short-term and disappointments often trigger significant negativity and selling activity when valuations are stretched. A feature of the high concentration in US equity markets is that the seven largest tech companies currently contribute a fifth of the S&P 500’s total earnings. Nvidia, which is expected to contribute almost a quarter of the index’s earnings growth in 2024, will report first quarter earnings this week in what is likely to be the next big test for the current market rally.

Although betting against these companies may seem risky short-term, the smart money in the long run will come from investing globally but selectively in companies with valuations that offer positive re-rating potential and downside protection.

All information as at 30/04/2024 unless stated.